×

The platform for the Entire Casting Industry

Partner

Foundry Corporate News

Topic Lost Foam

World Report on Investment Casting

Lesedauer: min

| Bildquelle: www.investmentcasting.org

By Tim Sullivan, Executive Director, and Merrin Muxlow, Partnerships and Marketing Director, Investment Casting Institute (source INCAST)

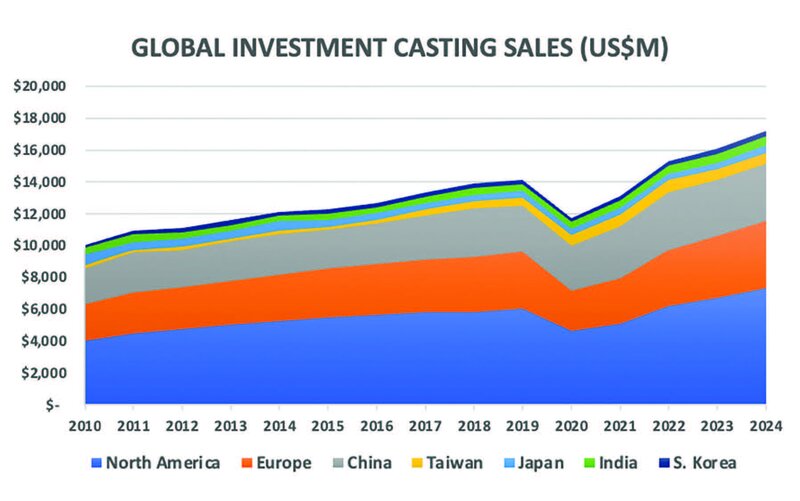

Executive Summary The global investment casting market enters 2025 with momentum in select sectors and regions, but the broader outlook is tempered by structural constraints and uneven demand. Total global sales reached $17.2 billion in 2024, led by high value-added applications across North America, Europe, and China.

Yet behind the top-line figures lies a story of sharp divergence—both by application and geography. High valueadded segments continue to flourish, while general industry and regional laggards drag on overall momentum. Aerospace, defense, and industrial gas turbines (IGTs) are expected to sustain strong growth in 2025, driven by persistent OEM backlogs, energy demands, and global military investment.

Automotive casting demand is expected to remain stable, supported by continued production of both internal combustion and electric vehicles. Key components—such as turbochargers, thermal housings, and drivetrain structures—remain essential across platforms.

Global automotive casting sales totaled $1.70 billion in 2024, with Europe,

China, and North America representing 71% of demand. EV growth and

policy incentives are reshaping component needs heading into 2025.

General industry castings, by contrast, face a more subdued outlook. Demand for parts used in pumps, valves, oilfield equipment, and industrial machinery is under pressure as infrastructure investment slows and global buyers gravitate toward lowercost suppliers. As a result, growth is increasingly concentrated in precision applications.

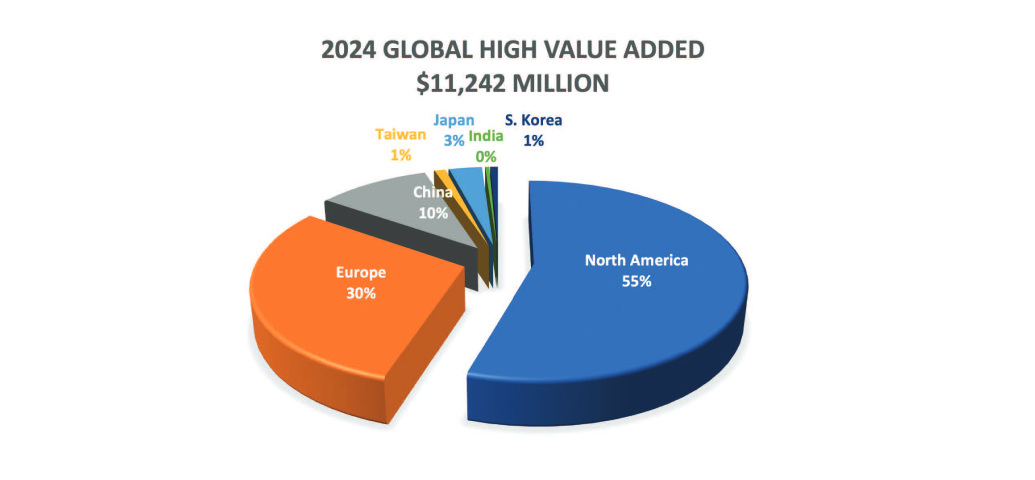

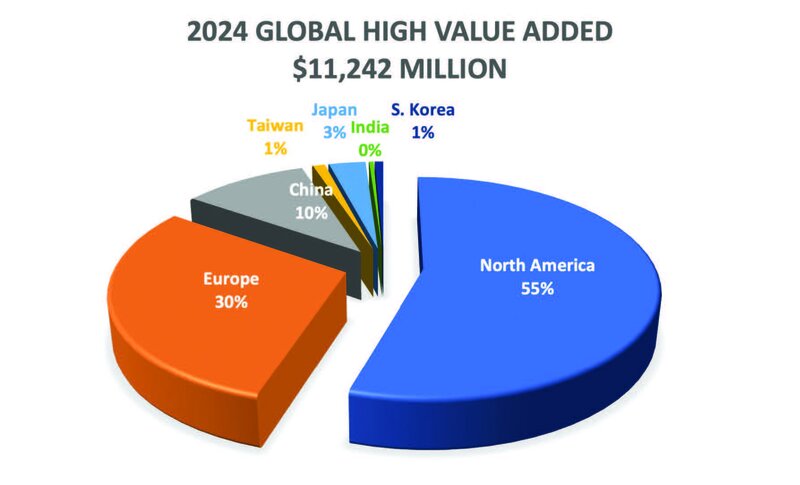

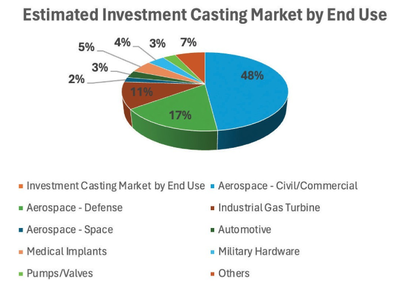

High-Value Added

High value-added applications, encompassing aerospace, defense, and industrial gas turbines, accounted for $11.24 billion in 2024—an estimated 65% of total global sales. North America led with $6.16 billion; Europe followed with $3.36 billion, and China contributed $1.15 billion. Together, these regions made up 94% of global high value-added casting revenue. Much of this demand is tied to aerospace recovery. Aircraft production has rebounded, with defense spending providing further support, particularly in the U.S. and NATO-aligned countries.

However, risks remain: aircraft OEMs face supply chain bottlenecks, and European defense spending is both politically sensitive and unevenly distributed. IGT castings showed moderate growth in 2024, though demand may soften in 2025 as power sector investment normalizes. Still, the long-term outlook remains bullish, particularly as AI-driven data centers drive demand for efficient, dispatchable energy sources.

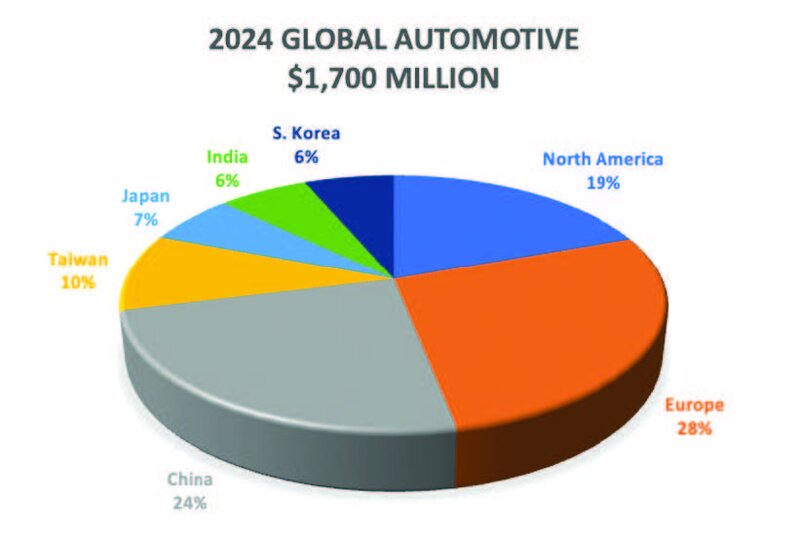

Automotive

Automotive casting demand held firm at $1.70 billion globally in 2024. Europe led with $468 million, followed by China at $410 million and North America at $330 million. Together, these three regions accounted for 71% of global automotive casting sales. Demand remains steady across automotive subsectors such as turbo wheels, rocker arms, and miscellaneous hardware. Platform consolidation and the transition to electric drivetrains are reshaping casting requirements. Lightweighting continues to displace some traditional components, even as EV-related thermal and structural castings create new demand. In Europe, emissions targets are driving the supply chain toward electrification. In China, domestic EV leaders like BYD are increasingly shifting production in-house, putting pressure on smaller casting suppliers.

North American OEMs are rebalancing internal combustion and electric vehicle production in response to evolving policies and tariff dynamics.

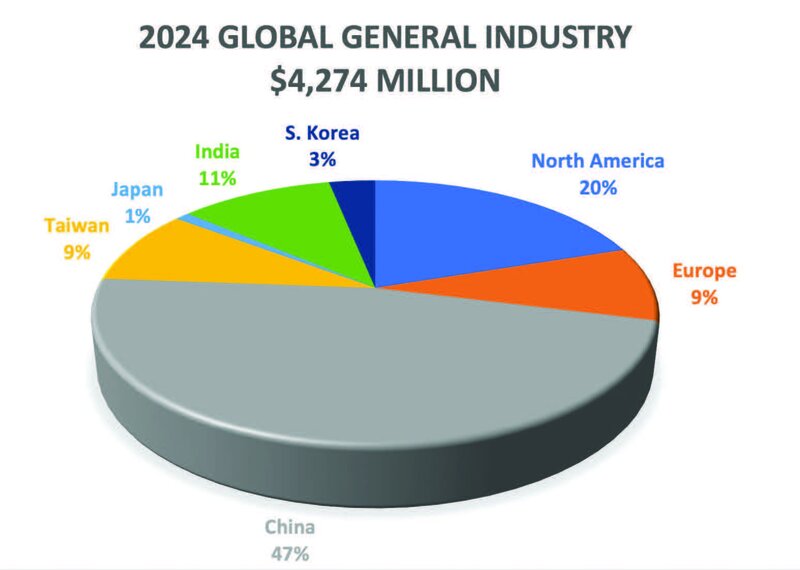

General Industry

General industry applications generated $4.27 billion globally in 2024, holding steady from the prior year. China led with $2.02 billion, followed by North America at $850 million and India at $450 million. Together, these three countries accounted for 76% of global general industry casting sales. This sector includes orthopedic implants, oil and gas components, medical devices, transportation, pumps and valves, and non-aerospace military hardware.

North America experienced moderate growth in oil & gas and medical implants, while China’s broader industrial slowdown weighed on demand. India’s continued rise reflects strong momentum in domestic manufacturing and defense programs.

Regional and Sector Leaders

Global market leadership remained concentrated in three regions:

- North America: $7.34 billion in total casting sales, representing nearly 43% of the global market. Notably, 84% of North American casting sales came from high value-added applications such as aerospace, defense, and industrial gas turbines.

- Europe: $4.21 billion, with the high value added sector playing a leading role in its casting market composition.

- China: $3.58 billion, with 56% of sales attributed to general industry castings, including medical devices, oil & gas, and non-aerospace military components. Together, these three regions drove nearly all net global growth in the investment casting industry. Elsewhere in Asia—including Japan, India, Taiwan, and South Korea—growth was modest and concentrated in niche sectors. However, the broader Asia- Pacific region, led by China and India, is expected to be a long-term growth engine. Accelerating industrialization, expanding domestic manufacturing, and increasing investment in defense and energy infrastructure are positioning the region for sustained momentum in investment castings.

applications now dominate, with growth increasingly concentrated in a few key regions and sectors.

Outlook

The industry is bifurcating, with highvalue sectors such as aerospace, defense, and industrial gas turbines (IGTs) driving growth, while other applications, particularly in general industry, show signs of stagnation. As reshoring, sustainability mandates, and energy transitions continue to reshape the landscape, demand for highperformance, precision castings will expand.

Precision castings remain at the forefront, particularly in highvalue sectors that require specialized components with tight tolerances. Leading producers in this segment are increasingly adopting digital transformation strategies—leveraging advanced automation, 3D printing for pattern making, and digital quality control systems.

Regional dynamics are also playing a key role in shaping the future of the market. North America, Europe, and China continue to dominate, with North America leading the charge due to its focus on high-value applications.

However, these regions will increasingly be challenged by rising competition and the shifting global supply chain dynamics. The Asia-Pacific region, particularly China and India, is poised for renewed growth.

Investment Casting Institute

About Merrin Muxlow:

Merrin is a marketing and research leader with deep expertise in the industrial sector, particularly casting and advanced manufacturing. She heads partnerships for the Investment Casting Institute and serves on the boards of the Investment Casting Foundation and the METAL for America Advisory Council. As both a strategist and author, she brings perspective on the full industrial landscape—from workforce development and supply chain resilience to technology adoption in foundries.

About Timothy Sullivan

Tim brings more than 30 years of leadership experience in the investment casting industry, most recently serving as Vice President of Corporate Affairs and Services at Hitchiner Manufacturing. Beyond his industrial leadership, Tim has held trustee roles with the Aircraft Builders Council and several healthcare organizations in New Hampshire, underscoring his commitment to both industry advancement and community impact. Tim’s deep expertise, strong industry relationships, and strategic vision make him well-positioned to lead ICI into its next chapter.

Source: www.investmentcasting.org

Firmeninfo

Investment Casting Institute

1 Paragon Drive, Suite 113

NJ07645 Montvale

Telefon:

E-Mail:

info(at)investmentcasting.org

Web:

www.investmentcasting.org

Verwandte Artikel

-

North American Investment Casting Performance and Outlook

zum Artikel

-

Japan – All Eyes on the 16th World Conference on Investment Casting (WCIC2025) in Kobe

zum Artikel

-

Wall Colmonoy Ltd (UK) Invests £2 Million in Advanced Vacuum Precision Investment Casting Capability

zum Artikel

-

Foundry of Excellence – Doerrenberg Edelstahl GmbH: Precision and Expertise in Casting Production

zum Artikel

-

Timothy Sullivan appointed new Executive Director of the Investment Casting Institute

zum Artikel

-

Pendulum Cutting Center PTC from Reichmann: Efficient Solution for Investment Casting Finishing

zum Artikel

-

EICF 2025 Conference in Liverpool – Investment Casting Sees Above-Average Growth

zum Artikel

-

Liverpool is calling – 32rd EICF International Conference & Exhibition 2025

zum Artikel

-

Investment Casting International Conference 2025 in Liverpool

zum Artikel

[515]